The Increasing Cost of Consumer Startups

If you have the dubious distinction of spending as much time around consumer facing seed VCs as I do, you likely start or end every conversation with some variant of “what’s exciting you these days?” And for the first time in my nearly 5 years in venture, the answer for the past six months has inevitably echoed some variant of “it’s been slow.” So what is going on?

The narrative for the past several years has been that the proliferation of cloud services, AWS in particular, has vastly reduced the cost of getting a startup off the ground. But I believe the low cost days have rather abruptly come to a halt – at exactly the wrong time. Not because AWS is suddenly expensive, but because the types of consumer behavioral shifts now being targeted are fundamentally more expensive.

Although I’ve been socializing this for a few months internally and amongst peers, I finally mustered the courage to write this piece after reading Sam Lessin’s Era of Lean Startups Comes To An End and Michael Eisenberg’s The Big Disruption.* Recode’s The App Boom is Over also plays a supporting role. Here’s the punchline: the low tech, low cost, low hanging fruit of the digital (and subsequently, mobile) era – digitizing or mobilizing offline to online processes – are coming to an end**. And until the next great platform or behavioral shift, the costs of innovation will be material higher. As we used to say in my card playing days, “the price of poker just went up.”

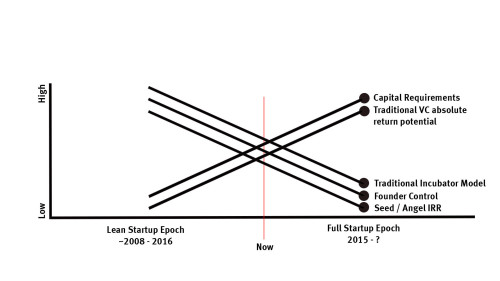

Here’s how Sam Lessin, writing at The Information puts it (pretty graph and all):

large_b86bb070-8d14-4469-9cf6-74ca9dffe636

For the past 10 years or so, startups have had two defining characteristics. First, they cost almost nothing to start. The intersection of good open-source software, infrastructure as a service, inexpensive distribution, and some plug-and-play monetization options like Google’s Adwords or an app store put all the power in the hands of small technical teams.

Second, when something worked—as rare as that was—the ability to scale and create extreme value very quickly was unprecedented…

But things are changing once again. Open-source software and infrastructure as a service will remain cheap forever. But the low-hanging fruit of highly scalable software startups has mostly been eaten. The winners in areas like media, messaging, advertising, and games have been established.

The next big opportunities seem to be shaping up around things like self-driving cars, on-demand services, VR, bots, bio, drones. But such opportunities lack turnkey generic infrastructure which enables development costs to drop close to zero. They are all expensive games in which to participate.

And Michael Eisenberg, founder of Israel-based Aleph takes it one step further:

Much of the next level of innovation will play out in the physical world, the financial markets and the world of experiences. Those innovative companies will take more money up front and they will become ever larger parts of VC portfolios.

I actually think Eisenberg gets even closer to nailing the emerging reality than does Lessin. For example, on demand services are expensive to scale, but cheap to launch. Bots are inexpensive to code. A lot of drone infrastructure is commoditized and modular at this point. Etc. But there are certain assets that are immutably capital intensive: real estate, logistics, banking, just to name three.

Let’s take the future of transportation for example (old timers might call this “logistics”). Boom is building the next generation of supersonic jets in a hanger outside of Denver. An actual real life jetplane. That is inherently capital intensive. The TSA/airport disrupters, as related in the WSJ’s All You Can Fly Experience, either purchase planes outright, lease planes, or pre-book large amounts of latent inventory – all demanding large upfront capital commitments. Turns out, putting a physical plane into the air is pretty darn expensive. Other next gen transport cos such as the Hyperloop raised $11M out of the gate to prove a prototype and another $80M soon after with a working test run. Good luck as a MicroVC.

Or, let’s take the reimagination of living. Whether its co-living operators such as WeLive and Common or subscription based flexible living models such as Roam, these companies also demand large upfront leasing obligations and build out costs. The paradox for seed investors is that a traditional seed round of a couple million dollars really only provides for a single (or at most, a couple) leases – all of which remain below full utilization for many months, constraining growth and economics. Want to bet on tiny homes or e-commerce driven pre-fab modular homes? That comes at a price too: Bluhomes raised $11M to launch its prototypes, and tiny home networks such as Kasita and Montainer also demand heavy prototyping and manufacturing costs to scale up their networks. ***

Even the millennial-first ecommerce brands (Bonobos, Trunk Club, Warby Parker, Baublebar) have, over the past several years, shown an increasing disposition towards brick and mortar exposure to combat clogged online acquisition channels. Not to mention a significant push from investors into private label inventory in order to boost otherwise anemic contribution margins across the sector. Stores. Inventory. All material overhead costs. And early in a company’s lifecycle too.

If, as Eisenberg suggests the “next level of innovation will play out in the physical world," there is likely to be a bifurcation of the seed stage funding stack. Strategic angels still have a place as founders may need $500k-1M to show an MVP, prove one element of the technology, and surround themselves with credible advisors. But the emerging world of capital intensive or asset heavy companies puts a material strain on the $25-50M MicroVC funds who are most comfortable writing $250-750k checks into $1-2M funding rounds.

Sure, these rounds may still occur, but they won’t be as a frequent. Future funding requirements for those businesses – often in breakneck succession – might well crush the model. And, at a minimum, only the MicroVCs with the absolute strongest upstream brands will survive. These VCs will have two options: ship checks into far larger rounds ($7-15M) with a similar risk profile or target more incremental, derivative companies with lesser upside and more balanced financing needs. The shift is occurring “at exactly the wrong time” – right when hundreds of seed funds have recently been raised.

Of course, of course there are still amazing, cash efficient, asset-light opportunities across consumer sectors. But, anecdotally, they are harder to discern and appear less frequent. Irrespective, these more physical/experiential companies represent bold bets on the future – and investors had better come to terms with it. For better or worse, the price of startups has just gone up.

* Tomasz Tonguz at Redpoint released “The Decline of New SaaS Company Formation” this morning with data suggesting that new SaaS companies are being started with reduced frequency in 2015 & 2016. It’s likely the same “low hanging fruit” argument could be applied to traditional SaaS (non AI/ML, chatbots, etc) as well, as Tomasz notes: “The key systems of record in SaaS are already in place. Salesforce, Netsuite, Marketo/Eloqua/Pardot/Hubspot, Zendesk. Subverting those incumbents is going to require a meaningfully better product or substantially more effective customer acquisition channel.”

** Grubhub and Opentable are two quintessential examples of this transition. Whereas in an offline world, one might pick up a phone and call a restaurant to book a reservation or order food delivery, Opentable enabled that process to be fulfilled via frictionless point and click. Many of these digitization transitions, including our investment in Spothero, have the additional benefit (and value creation) of opening up highly opaque inventory, thereby increasing frequency.

*** One could make the case that startups can offset these overhead costs via pre-order/pre-sale/Kickstarter revenue.