In Pursuit of Non-Linear Growth

It’s hard to imagine much can be added to the discussion around marketplace theory and metrics. And yet there’s a concept – an obvious one – that rarely seems to be referenced - and is one of the main drivers of our investment thesis at Chicago Ventures: searching for non-linear growth. It’s a characteristic that exists at Kapow, Shiftgig, Spothero and Curbside in our portfolio, amongst others and is extraordinarily powerful in early stage marketplace growth.

The Core Theory:

From what we’ve observed, non-linear growth is typically spurred by relationships on one side of the marketplace that allow it to launch and scale seamlessly across multiple new markets with compounding efficiency. In our experience (the companies listed above) that works best in geo-scaling marketplaces – because of the successive new market launches – where instead of building a new market from scratch in each new geography, one half of the market comes already solved at launch.

So for example:

As Kapow launches its real-time corporate events booking marketplaces in new cities, its demand side is pre-stimulated. How so? Because it works with large enterprises such as Google, HP, Deloitte, etc who boast dozens of regional offices, it can launch new cities featuring those clients with minimal sales effort.

As Shiftgig rolls out its on-demand temp labor booking marketplace from city to city, its demand side is also pre-stimulated by large national clients, for example a national big box retailer or hospitality provider that has temp needs in dozens of cities across the US.

Spothero is able to turn on new cities effectively overnight because of its enterprise partnerships with the largest parking operators in the country. While new entrants might have to put boots on the street in each new city to try and sign independent lot operators, Spothero can aggregate a large supply of inventory from its existing partners in the top cities in the country.

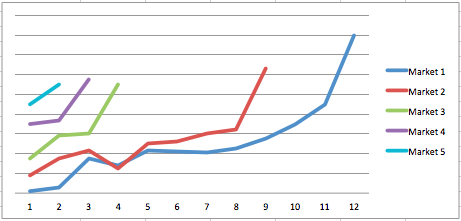

The benefit to this model is that it allows each new market to launch with incremental traction above each prior market launch. For example, here’s a breakout of one of our marketplace investments and each market growth (numbers have been changed slightly to protect confidentiality):

Graph1

This graph reflects months from launch to hitting an arbitrary revenue milestone, represented by the bold line. In this case, it took market 1 over 11 months and took market 4 only 2 months.

Let’s be clear: every marketplace wants to show a similar graph (reduced time to X) whenever they’re launching new markets – whether that be new geographies or new verticals, whatever. And many are able to show that, even starting from a base of zero because their playbooks have become well refined and each incremental launch has a faster growth rate than the prior.

But by betting on non-linear growers, we feel that companies can reduce the risk incumbent in new market launches because they start from a non-zero base.

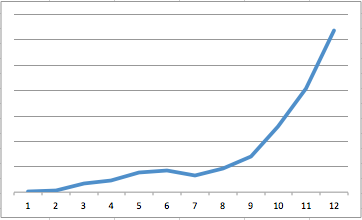

By aggregating these markets together, you yield a growth curve that begins to look extremely compelling:

Graph2

And each successive market launch will start at a compoundingly higher base – enabling the growth curve to bend closer and closer to a 90-degree angle.

When you understand this, it may not surprise you that the majority of our marketplace investments have some b2b component – simply because few customers can scale purchasing or selling across multiple markets (whether that is geographies or verticals). Even consumer facing companies such as Spothero and Curbside, whose end customer is a mass-consumer, have strong b2b relationships on the supply side, with lot operators and big box retailers, respectively.

Umm….so what about Uber?

Yeah – it’s a good point. Airbnb too. The two greatest digital marketplaces of the past decade are both built on seemingly linear growth (in that there was no supplier or buyer that could drive outsized liquidity in new city launches).

When I considered this issue for some time, I came to the following two observations:

Both of these platforms benefitted from unprecedented levels of virality and PR. And they deserve all the credit in the world for that. The consequence of that virality is, for example, that in Uber’s case, they were able to methodically selected new market launches by analyzing latent demand – the # of times the app had been opened in geographies where they weren’t operational. Understood this way, they actually weren’t starting from a base of zero at all because there was latent, pre-stimulated demand in each new geo (whose customers simply needed an e-mail or notification to alert them of the launch).

Both of these platforms enabled micro-entrepreneurship in that an enterprising supplier could purchase cars for others to drive or property managers could list multiple properties (or purchase others specifically for Airbnb) so that the supply side was not growing on a 1+1 incremental basis.

With these understandings, Uber/Airbnb actually are non-linear growers, and their greatness is that they achieved that from a harder to scale base.

But no matter how you look at it, it’s hard to build a liquid market. At Chicago Ventures, we feel there’s a benefit – or even a greater margin of error, so to speak – by focusing on companies that can pre-solve for one half of the market. And that said, I’d give anything to be an investor in Uber :)