"I'm only looking for billion dollar outcomes." Why that's absurd & why it's not :-/

Mazel tov technology world. Yesterday (March 31st) you minted two new unicorns: Sprinklr & Tanium. The former's fundraise elicited my favorite tweet of the day:

So if @Sprinklr is now valued at $1 billion, can it please buy a vowel?

— Alex Konrad (@alexrkonrad) March 31, 2015

But in all seriousness, according to the Wall Street Journal, those fundings bring the number of billion dollar companies to eighty.

So why should you, Ms. Aspiring Entrepreneur care?

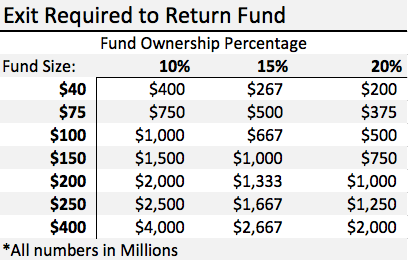

I hear lots of other VCs say casually or even in direct feedback "I don't think your company has billion dollar potential." Personally, I initially thought that benchmark was absurd - even if you accept Peter Thiel's power law hypothesis that you should only make investments that can return the fund. For a MicroVC such as Chicago Ventures (and there are now more than 200 of us!) investing out of our $40M first fund, if we own 10% of a company that exits for $400M, we return the fund. Own 15% and a sub $300M exit gets us to the promised land. Own even more and you get the idea. Take that you bigtime, arrogant, Midas List VCs...I will darn well invest in $300M companies!

And then we started learning that our mathematics didn't actually work in practice. The problem is that nearly every company we invest in will require more than our $2-3M of seed capital. As an exercise, let's assume that Company X, which has the potential to be a healthy $350M company, is growing nicely on a $3M seed round. It wants to tap Series A investors for a $10M round at a $30M pre-money valuation ($40M post). That means Series A investors, under a best case scenario, will see a <9x return on their money.

Series A investors should be thrilled to return 9x their money...right? Not quite. Anecdotally, I'd estimate that most top tier institutional A round investors are still looking for 25-50x upside on their money in an investment. Empirically, let's return to our exercise. Tier 1 Series A Investor invests $10M at $40Mpost, and voila, Company X kills it and exits for $350M. Series A investor returns $87.5M which, on a $250M fund, is barely a third of the fund. Oops?

ExitReqtoReturnFund

What we've proven is that there's an economic disconnect between Seed investor threshold and Series A investor threshold. If we had more time, we could repeat this exercise for A round to B round, B to C, etc. You'd find the same tension. In fact, if you analyze the above graph, you'll note that MicroVC funds (sub $50M) have zero minimum returns overlap with Series A funds >$150M. That is what's powering the disconnect.

So what happens to Company X? Often Company X is actually a really good business - with strong leadership, traction and economics. In those cases, Company X is generally able to tap either lower tier institutional VCs or non-institutional money: corporate (strategic) venture, HNWI, or private family offices. That is OK, conceptually, but it generally doesn't make CEOs happy and it can be a challenge for us to explain to the investors in our fund as well.

As a friend to entrepreneurs, this setup is frustrating. But it is the reality. If there are any suggestions from the crowd on how to bridge this gap, I'd love to hear how other funds or investors are handling it. One obvious answer: Raise a larger fund so you can support companies through later rounds. As a 3 year old startup ourselves, we don't quite have the track record to do that yet - but it's certainly something we're thinking about.

I broke my rule again and wrote about VC. Oh well :(

Till next time,

Ezra